Unlocking the Latest Real Estate Trends: Insights from S&P/Case-Shiller's Home Price Index and Northwest MLS Report for February 2024

On February 27, 2024, S&P/Case-Shiller published the Home Price Index data for December 2023, shedding light on the real estate market's performance last year. A significant observation was that all 20 markets showed positive year-over-year gains, including Portland, which had previously been below the national trend. Additionally, half of the markets in the US reached all-time highs, surpassing historic averages, signaling a trend of accelerating housing price gains at the national level.

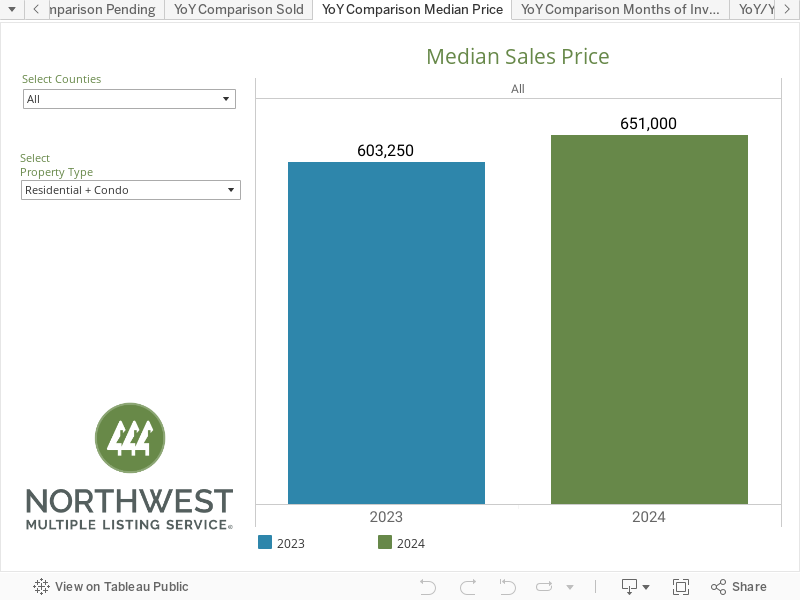

Per the Northwest MLS report, the real estate market in Washington remained in line with expectations at the conclusion of February 2024. Mirroring the traditional seasonal trend during winter, alongside elevated interest rates, the month experienced a subdued pace of activity. The average interest rates lingered at 6.94% throughout the past month, constraining both potential buyers' affordability and sellers' reluctance to relinquish low-rate mortgages. Within the Washington counties serviced by the Northwest MLS, February 2024 marked a nearly 2% decline in closed sales transactions compared to the previous year. Nevertheless, median prices sustained an upward trajectory, displaying a year-over-year surge of close to 6%.

According to Trendraphix’s recently released (month-to-date) March data, there was a 23.4% year-over-year increase in pending sales in the four-county (King, Snohomish, Pierce, and Kitsap County) region. The spring sales season has kicked off early this year, promising more activity and indicating pent-up demand.

Here’s a snapshot that closely matches how the S&P/Case-Shiller Home Price Index is measured for resales only of single-family homes in the four-county area (not new construction and not including condominiums or land):

“U.S. home prices faced significant headwinds in the fourth quarter of 2023,” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices. “However, on a seasonally adjusted basis, the S&P Case-Shiller Home Price Indices continued its streak of seven consecutive record highs in 2023. Ten of 20 markets beat prior records, with San Diego registering an 8.9% gain and Las Vegas the fastest rising market in December, after accounting for seasonal impacts.”

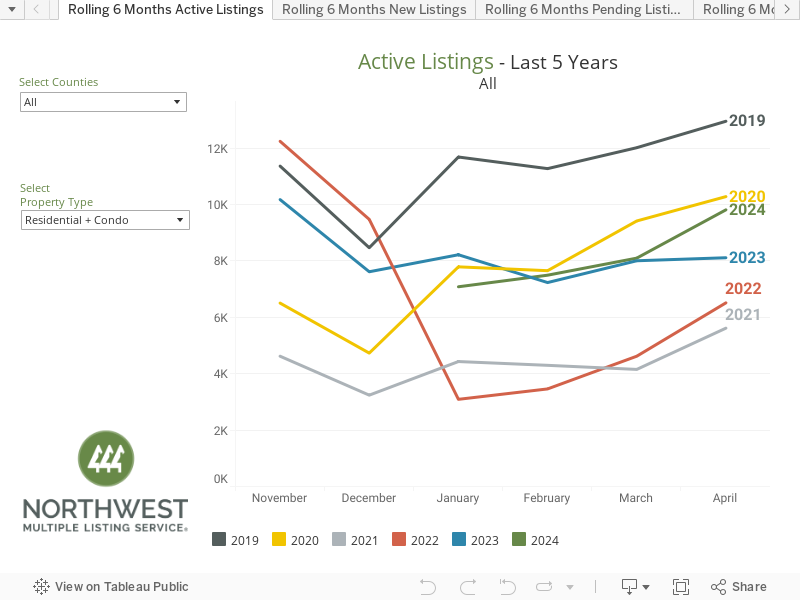

The Seattle metro area finished 2023 with a modest 3% median home price increase, and the West Coast in general was a late bloomer to recover after witnessing some of the most significant declines in recent years, but, again, that followed the most significant gains during the pandemic. While this has been a yo-yo, it seems clear that waiting to buy will mean more competition and higher prices. In the four-county region in February 2024, there were 1.2 months of inventory, which is down 13.8% year over year. However, compared to January, which had 2,848 listings, the number of new listings was up in February with 3,840 listings. Dean Jones, President and CEO of Realogics Sotheby's International Realty and advisors expect to see a surge of new listings this spring, but also more enthusiastic sellers testing higher prices.

Over a February weekend, RSIR encountered an Eastside view property that attracted over 250 tours and drew 9 competing offers before being signed under contract. This scenario is not unique, with open house activity in sought-after locations attracting numerous prospective buyers. The scarcity of housing inventory is evident, and it's clear that new construction is struggling to catch up with the regional housing demands. As a result, this imbalance is expected to drive prices even higher in the near future. Waterfront and waterview homebuyers are feeling the pinch of low inventory throughout the Seattle area especially in desireable locations such as Bainbridge Island.

Many homebuyers are observing the buy-then-refinance strategy, and it’s clear that after prices reset to digest higher mortgage interest rates, we will witness a new cycle. We expect the inventory to increase substantially in the next few months but with higher pricing. As of February, the median sales price is $725,000 in the four-county region, showing price growth despite the cooler winter market.

It appears the real estate market has transitioned from a mindset of "FOMI" (fear of mortgage interest) to "FOMO" (fear of missing out). While buyer demand may not have decreased, it seems to have been postponed. Just as the historically low mortgage rates in 2020 and 2021 accelerated future demand, the period of 2022 to 2023 experienced a shift in demand, which is now rebounding. This rebound can be attributed to the realization that although higher mortgage rates bring about a temporary financial challenge, the enduring advantage lies in securing a better purchase price. With home prices continuing to increase by 3% or more, these gains help offset the impact of higher rates in the long run.

Median Sales Price

Historical Real Estate Statistics | Information and statistics compiled and reported by the Northwest Multiple Listing Service.

In navigating the dynamic landscape of the real estate market, it's essential to have an experienced guide who can interpret the data and trends. As a seasoned real estate broker, Danny Varona is ready to assist you in understanding the information provided in this report. From the insights gleaned from the S&P/Case-Shiller Home Price Index to the nuanced analysis of local market conditions, my expertise can help you navigate the complexities of buying or selling a home with confidence. Don't hesitate to Reach out, and let's work together to achieve your real estate goals amidst this ever-evolving market. I'd love to guide you through your next real estate journey.